Five factors that impact your credit score

Your credit score signals to banks, lenders, landlords and even potential employers how good you are at paying back the money you borrow. The higher your credit score, the better your chances you’ll be approved. Learn the factors that make up your credit score to better understand and improve your credit score.

Think of your credit score as a report card for how you handle money. It signals to banks, lenders, landlords and even potential employers how good you are at paying back the money you borrow. The higher your credit score, the better your chances you’ll be approved.

Building a better credit score starts with understanding credit scores – and what makes a score go up and down.

Your credit score is based on the information in your credit report, including your payment history, the amount of debt you owe, how long you’ve been using credit, new or recent credit, and the types of credit used. FICO® is the most widely used score, but there are other credit scoring companies. Scores may vary slightly from one company to the next.

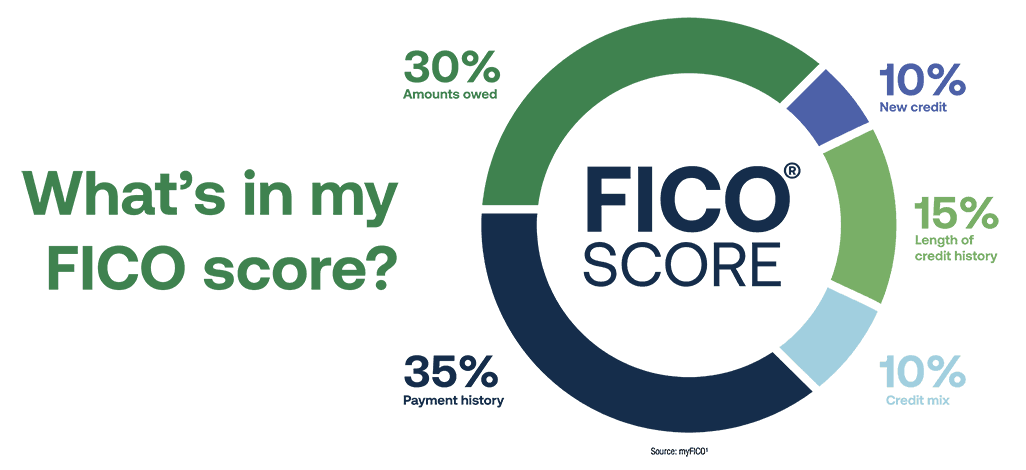

Here are the top five factors that make up your credit score.

1. Payment history

Paying your bills on time is the most important thing you can do to build your credit score because your payment history makes up 35% of your FICO score. Information on late payments, bankruptcies, and collection accounts are also considered.

Using autopay, which automatically pays your bills from your bank account each month, can help prevent late payments, along with monthly reminders on your phone to check and pay your bills. Also, look at your due dates to make sure your payment will post on time.

2. Amounts owed

Your credit utilization rate refers to how much of your available credit you’re using – how much you owe. For example, if your credit card limit is $10,000 and you’ve used $3,000, your credit utilization rate is 30%. A low rate signals to lenders that you aren’t overspending.

Paying down your debts and increasing your credit limits will help you improve your credit utilization rate, which generally accounts for 30% of your FICO score.

3. Length of your credit history

How long you’ve had credit accounts open in your name makes up 15% of your FICO score. This includes the average age of your accounts, the age of your oldest account, and how long it’s been since you opened an account. If you’re new to using credit, it may take some time to build your credit history.

Keep in mind, if you close an old credit card account, it will reduce your credit history length. And if you open several new accounts, it could lower the average age of your accounts.

4. Credit mix

Lenders want to know you’re able to handle and pay back different types of credit. That includes installment loans, such as mortgages and car loans with fixed payments over a set time, and revolving credit, including credit cards or home equity lines of credit that have different monthly payments based on how much credit you use. The various types of credit accounts you have make up 10% of your FICO score.

While having a healthy mix of credit is good, applying for loans or other debt just to diversify your credit isn’t. Your credit mix is a small part of your credit score, so any changes you make probably won’t have a significant impact.

5. New credit

Every time you apply for new credit, a lender or creditor requests your credit report and it shows up as a hard inquiry (sometimes also called a hard pull or hard credit check) on your credit report. New credit makes up 10% of your FICO score.

You likely won’t see much of a dip from a single hard inquiry, but several in a short time can cause more damage to your score. That’s because trying to open several new accounts in a short time could suggest you’re struggling financially. However, most credit-scoring systems give consumers a window of time, typically from 14 to 45 days, to rate shop for a mortgage or auto loan. During this period, all hard credit checks for the same type of loan count as a single inquiry.

On the road to a better credit score

Knowing how credit scores work is the first step to improving your score – and your chances for being approved the next time you apply. Use free credit check services to monitor how your financial decisions are impacting your credit score. You can also request an annual free copy of your credit reports from each of the three major credit bureaus (Equifax, Experian, and TransUnion).

(1) What’s in my FICO Score? MyFICO.

(2) Not all applicants are approved. While no credit history is required, Snap obtains information from consumer reporting agencies in connection with submitted applications, and your score with those agencies may be affected.