What is FICO? All you need to know

Understand your FICO® score and how it impacts your financial health. Learn what a FICO score is, how it’s calculated, why it matters, and how to improve yours.

Key takeaways

A FICO score is a type of credit score. It’s a three-digit number designed to predict the likelihood of on-time repayment.

The FICO score range runs from 300 to 850. Higher scores generally indicate lower credit risk.

Most lenders rely on FICO scores. FICO is the most commonly used credit scoring model in the U.S.

What a FICO score means is determined by five factors. Payment history, credit utilization, length of credit history, new credit, and credit mix all influence your score.

You can check your FICO score without hurting your credit. Reviewing your own score has no impact on your FICO score.

What is a FICO score?

If you’re asking ”What is a FICO score?”, you’re really asking about one of the most important measures of credit risk used today.

A FICO score is a three-digit number that summarizes your credit behavior and represents your level of credit risk. In simple terms, it helps answer the question lenders care about most: How likely are you to repay credit on time?

It’s important to understand that a FICO score is one specific type of credit score. While other scoring models exist, FICO scores are the most widely used by lenders.

When people ask what a FICO score is, they’re usually asking how lenders view their creditworthiness and how that number affects approvals, rates, and terms.

What does FICO stand for?

FICO stands for Fair Isaac Corporation, the company that developed the FICO credit scoring model.

When people ask what FICO means, they’re referring to this scoring system and the methodology behind it. Since its introduction in 1989, the FICO model has become the industry standard for evaluating credit risk.

How is a FICO score calculated?

To understand what a FICO score means, it helps to know how FICO scores are calculated. The FICO score range spans from 300 to 850 and is based on five weighted factors:

Payment history (35%)

Payment history reflects whether you’ve paid credit obligations on time. Late or missed payments can significantly lower a FICO score.

Amounts owed / credit utilization (30%)

This factor measures how much of your available credit you’re using. Lower utilization generally supports a higher FICO score.

Length of credit history (15%)

Longer credit histories provide more data about how you manage credit over time.

New credit (10%)

Opening multiple accounts in a short period can indicate higher risk and may lower your score temporarily.

Credit mix (10%)

Using different types of credit responsibly can have a modest positive effect on your FICO score.

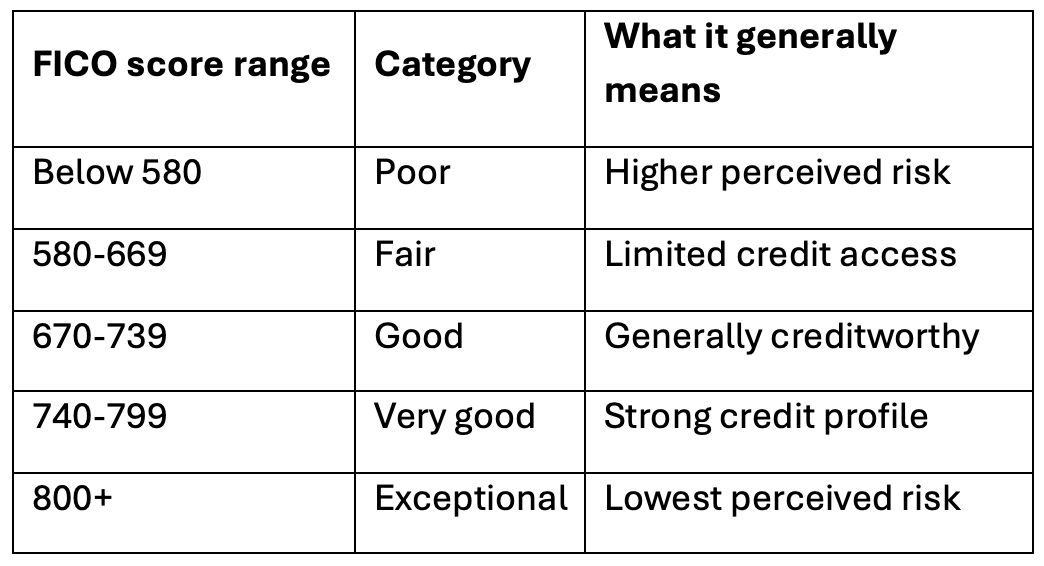

What is a good FICO score?

Looking at the FICO score range helps clarify what a FICO score means in practical terms.

Moving higher within the FICO score range can affect interest rates, credit limits, and approval decisions.

Why your FICO score matters

A FICO score influences many financial decisions, not just loan approvals.

Lenders use FICO scores to assess risk, while other organizations may rely on them to help set terms or conditions. A stronger score can result in:

Lower interest rates

Higher credit limits

Greater access to credit

Understanding what a FICO score means can help you anticipate how your credit profile may be viewed.

Which FICO score do lenders use?

There isn’t a single universal FICO score.

Different lenders may use different FICO score versions depending on the type of credit involved, such as credit cards, auto loans, or mortgages. This is one reason consumers often see multiple FICO scores at the same time.

Even though the numbers may vary slightly, all versions are designed to measure the same core risk: likelihood of repayment.

FICO vs. VantageScore

FICO is not the only credit scoring model, but it is the most widely used.

FICO and VantageScore use similar data and share the same 300-850 scale. However, lenders rely far more heavily on FICO scores when making decisions.

When someone asks “What is FICO?” they are typically asking about the score lenders use most.

How to improve your FICO score

Improving a FICO score takes time and consistency.

Pay bills on time

Keep balances low

Avoid opening many new accounts at once

Maintain older accounts when possible

Positive habits tend to show results gradually rather than immediately.

How to check your FICO score

You can check your FICO score without damaging your credit.

Checking your own score is considered a soft inquiry and has no impact to your FICO score. Reviewing your score regularly can help you track changes and spot potential issues early.

Frequently asked questions about FICO

What does FICO stand for?

FICO stands for Fair Isaac Corporation.

Is a FICO score the same as a credit score?

A FICO score is one type of credit score, and it is the most commonly used by lenders.

What is considered a good FICO score?

Generally, a score of 670 or higher falls into the good range within the FICO score range.

How often does a FICO score change?

A FICO score can change whenever new information is reported to your credit report.

Does checking my FICO score hurt my credit?

No. Checking your own score has no impact to your FICO score.

Does Snap Finance affect my FICO score?

In general, there’s no impact to your FICO score when you apply for Snap-branded pay-over-time options.

Why is my FICO score different across lenders?

Different lenders may use different FICO score versions or data sources, which can result in different numbers.

Final thoughts

Understanding what a FICO score is, what a FICO score means, and how the FICO score range works gives you clarity when reviewing your credit.

Your FICO score reflects patterns over time. With consistent habits, it can improve – and checking your progress regularly can help you stay on track.

Snap-branded product offering includes retail installment contracts, bank installment loans, and lease-to-own financing. Talk with your local Snap merchant for more details on which product qualifies at your store location. For more detailed information, please visit snapfinance.com/legal/financing-options